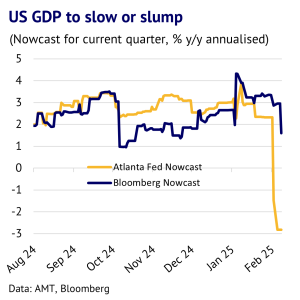

6 March 2025: The US economy has performed well in recent years, but is now facing some significant challenges. Higher import tariffs are expected across many industries, which is leading to a surge in goods imports before trade barriers go up. This is damaging US GDP prospects and the Atlanta Fed Nowcasting model is flagging up a potential recession this quarter. Also, inflationary pressures are building, with many US firms passing on higher prices. Base metal prices are getting a temporary boost from this, but the medium-term outlook is turning more bearish.

US Economy Heads Into Choppy Waters. With the arrival of Donald Trump in the White House, US economic policy around tariffs is changing daily and sometimes even hourly. Moreover, there is often little economic logic to these changes. This is making life incredibly difficult for companies trading with and in the world’s largest economy.

What seems clear though is that tariffs are going up for many goods and this has encouraged traders to rush shipments to the US, in the hope of arriving before the walls get too high. For example, this rush can be seen in gold, consumer goods, solar panels and industrial components. The ports of Los Angeles and Long Beach reported their busiest January on record.

The immediate problem with higher imports is that it is going to be a big drag on US GDP in Q1 and the Atlanta Fed Nowcasting model (based on advanced trade data for January) is predicting a potential recession. Another problem further ahead is that uncertain US policy could easily feed through into reduced business confidence and investment, which would be a medium-term headwind for US GDP growth. General Motors, for example, has said that it will delay future investments until it has greater clarity on government policy and the National Association of Home Builders is flagging up soft capital spending plans in February for its members.

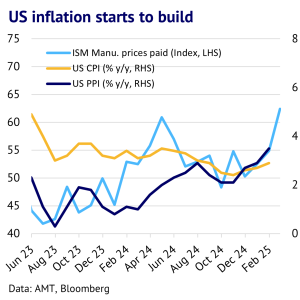

US Inflationary Pressures Are Building. Another economic challenge is that higher tariffs are starting to drive up US inflation. According to a survey conducted by consultancy firm EY-Parthenon, half of US firms plan to pass on two-thirds of higher input costs from tariffs. This is now being reflected in the ISM survey of manufacturing, which saw a 14% jump in prices paid in February. CPI and PPI figures are lagging, but seem to be picking up some early inflationary pressure in January. While there is hope in the White House that higher tariffs will drive a revival in US manufacturing, it will take several years for supply chains to fully adjust, particularly in industries like aluminium, copper and steel. This leaves consumers to bear the brunt of price hikes, eating into their disposable incomes. The next question is, what will happen to base metals if the US economy is hit by stagflation i.e. falling economic growth and rising inflation?

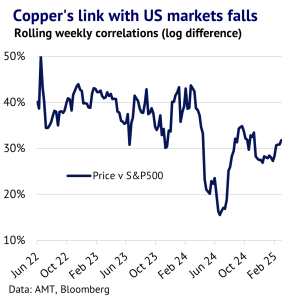

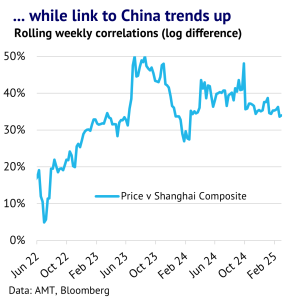

Base Metals Start to Delink from US Markets. The US is facing some challenging months ahead, and risk aversion can be seen, with the US S&P500 equity index down 5% m/m (data to 6 March). However, the base metal markets have been mostly ignoring this, with copper up 4% m/m. Partly this is because the recent equity rout was driven by tumbling technology stocks, but there has also been a broader change in drivers for copper. US equities have become less important and Chinese equities more important. As we show in our charts, copper’s rolling correlation with the S&P500 reached 50% back in June 2022, but since then has fallen back to around 30% at the end of February. Meanwhile, copper’s link with the Shanghai Composite Index has increased from 17% back in June 2022 to 34% at the end of February. While China dominates in terms of copper market fundamentals, investors play a key role as well through financial market sentiment. Commodities can also do well in an inflationary environment.

Copper prices to be hampered by weaker US sentiment. The stronger correlation between copper and Chinese equities implies that if economic growth in China continues at a decent pace, then copper prices will get some support, even if the US struggles. However, investor sentiment is likely to turn increasingly bearish in the months ahead. We are also mindful that the current tightness being seen in base metal spreads may well just be a short term reaction to US tariffs and there is lots of scope for this tightness to unwind, creating negative dynamics for fundamentals on a 3-6 month view. We are currently reviewing our forecasts for the base metals complex, but downside risks appear to be building.